Summary: Statistics empower business to make informed decisions by analysing data for market insights, forecasting trends, managing risks, and measuring performance. Leveraging statistical tools enhances budgeting, quality control, and competitive advantage, enabling organizations to optimize operations, respond to market changes, and achieve sustainable growth in a data-driven world.

Introduction

In today’s fast-paced and highly competitive business environment, data is the new currency. Every transaction, customer interaction, and market shift generate valuable data. But raw data alone is meaningless unless it is analysed and interpreted correctly.

This is where statistics come into play. Statistics provide the essential tools and methodologies that allow businesses to transform data into actionable insights, guiding decision-makers toward strategies that drive growth, efficiency, and profitability.

Whether it’s understanding market trends, optimizing operations, or managing risks, the importance of statistics in business cannot be overstated.

Key Takeaways

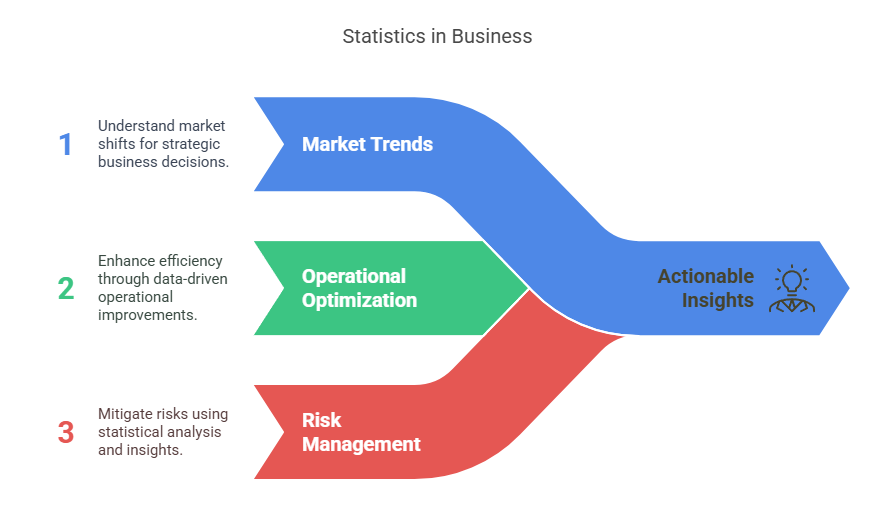

- Statistics transform data into actionable insights for better business decisions.

- Market research uses statistics to understand consumer behaviour and preferences.

- Forecasting relies on statistical models to predict future business trends.

- Risk management employs statistics to identify and mitigate potential threats.

- Advanced analytics powered by statistics provides a competitive business edge.

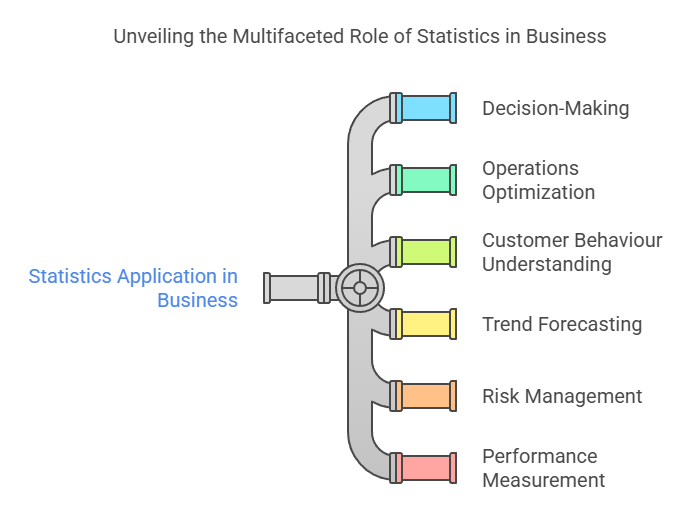

Statistics Application in Business

Statistics application in business involves using Data Analysis techniques to improve decision-making, optimize operations, understand customer behaviour, forecast trends, manage risks, and measure performance. These applications help businesses gain insights, increase efficiency, and achieve competitive advantages in dynamic markets.

Data-Driven Decision Making

One of the most significant shifts in modern business management is the move from intuition-based to data-driven decision-making. Statistics empower organizations to make informed choices by analysing empirical evidence rather than relying on guesswork. Statistical analysis helps managers evaluate options, predict outcomes, and choose strategies that are most likely to succeed.

For example, by analysing sales data, a company can determine which products are performing well and which are underperforming, allowing for better inventory management and targeted marketing.

Statistical tools such as regression analysis and hypothesis testing enable businesses to validate assumptions, measure the effectiveness of changes, and minimize the risk of costly errors. In essence, statistics transform uncertainty into measurable probabilities, making business decisions more rational and effective.

Market Research and Consumer Insights

Understanding customer needs and market dynamics is critical for business success. Statistics play a pivotal role in market research by providing the framework to collect, organize, and interpret data about consumers and competitors.

Techniques such as surveys, cluster analysis, and data mining help businesses segment their audience, identify buying patterns, and uncover emerging trends.

For instance, a company launching a new product can use statistical sampling to gauge consumer interest and estimate potential demand. By analysing survey data, businesses can identify which features are most valued by customers, enabling them to tailor offerings and marketing messages accordingly.

Additionally, statistics help measure the effectiveness of advertising campaigns, track brand perception, and monitor shifts in consumer behaviours, ensuring that businesses remain responsive and relevant in a dynamic marketplace.

Forecasting and Trend Analysis

Predicting the future is inherently uncertain, but statistics provide the tools to make educated forecasts based on historical data and current trends. Time series analysis, moving averages, and regression models are commonly used statistical techniques for forecasting sales, revenue, demand, and market trends.

For example, retailers use statistical forecasting to anticipate seasonal fluctuations in demand, allowing them to optimize inventory levels and staffing. Financial analysts rely on trend analysis to project future earnings and identify potential risks.

By leveraging statistical models, businesses can prepare for upcoming challenges, allocate resources more effectively, and capitalize on new opportunities as they arise. Accurate forecasting is essential for strategic planning and long-term sustainability.

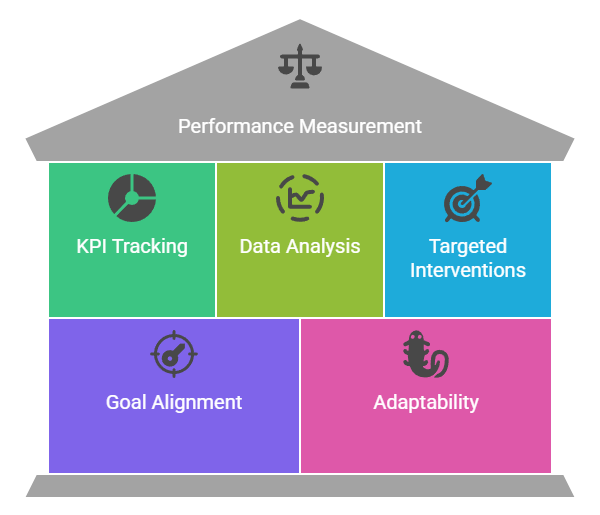

Performance Measurement and KPIs

Measuring performance is vital for continuous improvement and accountability. Statistics enable businesses to define, track, and analyses key performance indicators (KPIs) across various functions, including sales, marketing, production, and customer service. By quantifying performance metrics, organizations can identify strengths, pinpoint weaknesses, and implement targeted interventions.

For example, a manufacturing company may use statistical process control charts to monitor product quality and detect deviations from standards. Sales teams track conversion rates and customer acquisition costs to evaluate the effectiveness of their strategies.

Regular analysis of KPIs ensures that businesses remain aligned with their goals and can quickly adapt to changing circumstances. In short, statistics provide the objective benchmarks needed to drive performance and accountability at all levels of the organization.

Risk Management and Quality Control

Every business faces risks, from financial losses to operational disruptions. Statistics are essential for identifying, quantifying, and mitigating these risks. Statistical risk assessment involves analyzing the likelihood and impact of adverse events, enabling businesses to develop contingency plans and allocate resources more effectively.

Quality control is another area where statistics are indispensable. Techniques such as Six Sigma, control charts, and process capability analysis help organizations monitor production processes, detect defects, and maintain high standards of quality.

By applying statistical methods, businesses can reduce variability, minimize waste, and enhance customer satisfaction. Proactive risk management and quality control not only protect the bottom line but also build trust and credibility with stakeholders.

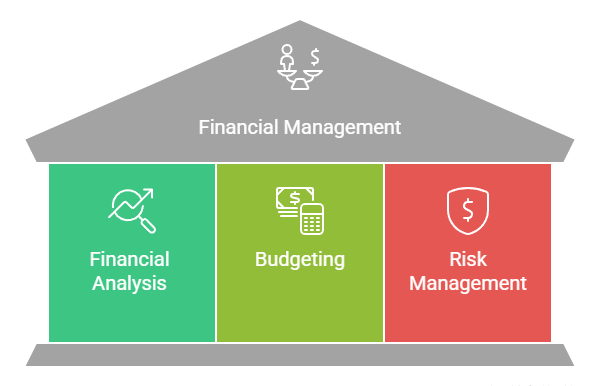

Financial Analysis and Budgeting

Sound financial management is the backbone of any successful business. Statistics play a crucial role in financial analysis, budgeting, and forecasting. By analysing historical financial data, businesses can identify trends, assess profitability, and make informed investment decisions.

Budgeting relies on statistical models to estimate revenues, expenses, and cash flows under different scenarios. Financial ratios, variance analysis, and predictive analytics help organizations monitor financial health, detect anomalies, and optimize resource allocation.

For example, banks use statistical credit scoring models to evaluate loan applications and manage credit risk. Investors analyze statistical indicators to assess the performance and volatility of stocks and portfolios. In all these cases, statistics provide the quantitative foundation for prudent financial planning and decision-making.

Competitive Advantage Through Analytics

In an era where data is abundant but actionable insights are scarce, the ability to leverage statistics for advanced analytics is a key differentiator. Businesses that harness statistical techniques for Big Data Analysis, Machine Learning, and predictive modelling gain a significant competitive advantage.

Analytics-driven organizations can identify emerging opportunities, respond swiftly to market changes, and personalize customer experiences at scale. For example, e-commerce platforms use recommendation algorithms based on statistical analysis of user behaviour to drive sales and enhance customer loyalty.

Supply chain optimization, fraud detection, and dynamic pricing are just a few areas where advanced statistical analytics create value and set businesses apart from their competitors. Ultimately, a strong foundation in statistics empowers organizations to innovate, adapt, and thrive in a rapidly evolving business landscape.

Conclusion

Statistics are the lifeblood of modern business management. From guiding strategic decisions and understanding markets to managing risks and driving performance, statistical methods are woven into every aspect of business operations.

As the volume and complexity of data continue to grow, the importance of statistics in business will only increase.

Organizations that invest in statistical literacy and embrace data-driven decision-making will be better equipped to navigate uncertainty, seize opportunities, and achieve sustainable success in the digital age.

Frequently Asked Questions

How Do Statistics Improve Business Decision-Making?

Statistics provide objective Data Analysis, enabling businesses to make informed decisions based on empirical evidence rather than intuition. This reduces uncertainty, minimizes risks, and increases the likelihood of achieving desired outcomes.

What Role Do Statistics Play in Market Research?

Statistics help businesses collect, analyses, and interpret market data, revealing consumer preferences, market trends, and competitive dynamics. This information guides product development, marketing strategies, and customer segmentation for better market positioning.

Why are Statistics Important for Risk Management in Business?

Statistics quantify the probability and impact of potential risks, allowing businesses to develop effective mitigation strategies. This proactive approach enhances resilience, protects assets, and ensures long-term stability and growth.

Authors

-

Written by:

Aashi VermaReviewed by: